Budget 2026 & Tax Reforms: Complete Guide

- Posted By Amritesh

- On June 22nd, 2026

- Comments: no responses

A deep-dive into income tax changes, the new Income Tax Act, GST and customs reforms, and a practical personal finance roadmap for FY 2026–27.

Introduction: A Budget of Consolidation

Finance Minister Nirmala Sitharaman presented her ninth consecutive Union Budget on February 1, 2026, making history while delivering a slate of tax reforms designed to ease compliance, reward the middle class, and usher in the most significant overhaul of India’s tax code in over six decades. With global headwinds intensifying — from tariff disputes to currency volatility — Budget 2026 struck a careful balance: sustaining fiscal discipline while putting more money in people’s hands.

For the individual taxpayer, the headline takeaway is stability. Income tax slabs and rates for FY 2026-27 remain exactly as they were under Budget 2025 — both under the new tax regime and the old tax regime. There is no slab tinkering this year. But that surface-level calm is deceptive. Underneath, a set of structural reforms — the activation of the Income Tax Act, 2025, changes to capital gains treatment, securities transaction tax hikes, customs duty rationalisation, and sector-specific relief — together reshape the financial planning landscape for salaried employees, retirees, investors, traders, and NRIs alike.

This guide walks through every major change in detail, explains what it means in practical terms, and closes with a structured action plan you can actually use before your next payroll declaration or ITR filing.

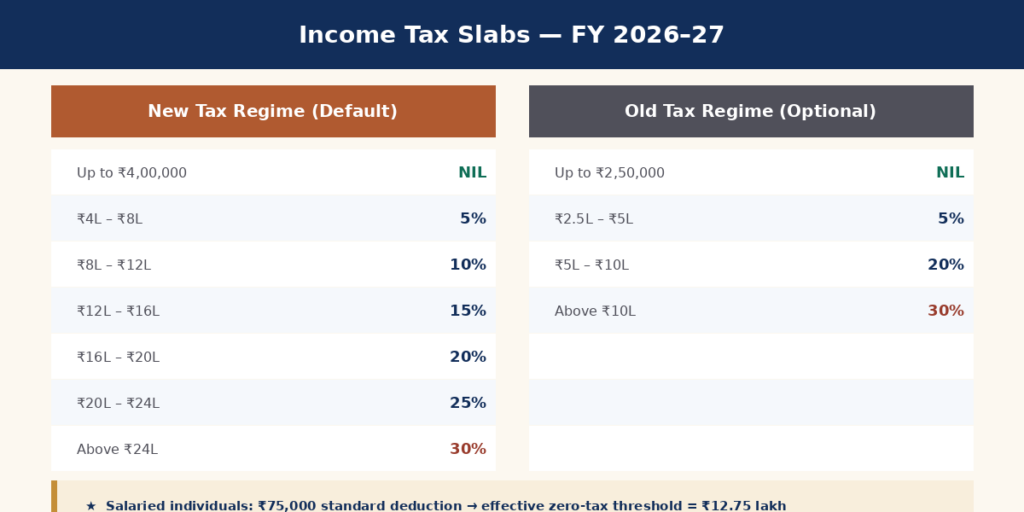

1. Income Tax Slabs: What Stayed the Same

Budget 2026 retained the revised income tax slab structure introduced in Budget 2025 under the new tax regime, which continues as the default option for all individual taxpayers. The old tax regime remains available for those who find it more beneficial — particularly taxpayers with significant deductions under Sections 80C, 80D, HRA exemption, and home loan interest.

New Tax Regime — FY 2026–27 (Default)

| Income Range | Tax Rate |

| Up to ₹4,00,000 | NIL |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Old Tax Regime — FY 2026–27 (Optional, under 60 yrs)

| Income Range | Tax Rate |

| Up to ₹2,50,000 | NIL |

| ₹2,50,001 – ₹5,00,000 | 5% |

| ₹5,00,001 – ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Higher Exemption for Senior Citizens (Old Regime Only)

The old tax regime continues to offer a higher basic exemption limit to resident senior citizens. For resident individuals above 80 years (super senior citizens), the basic exemption limit under the old regime stands at ₹5,00,000 — a full ₹2.5 lakh higher than the standard exemption. The new tax regime, by contrast, does not offer any age-based relaxation; the ₹4,00,000 exemption applies uniformly regardless of age. This is an important consideration for retirees deciding between regimes.

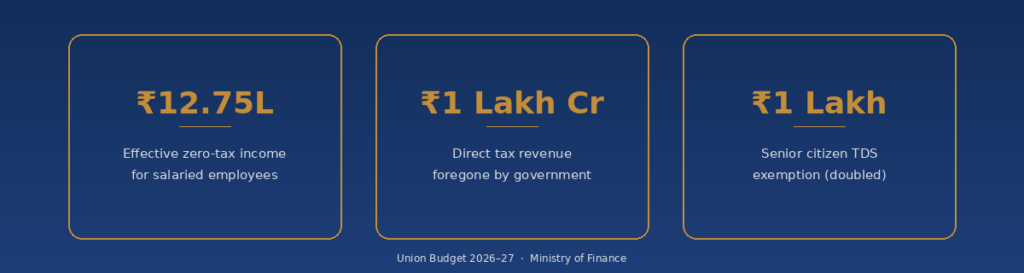

A critical detail for salaried employees: the ₹75,000 standard deduction under the new regime — up from ₹50,000 in earlier years — means income up to ₹12.75 lakh is effectively tax-free. The Section 87A rebate of ₹60,000, retained in Budget 2026, ensures zero tax liability for taxable income up to ₹12 lakh even without the standard deduction. Family pensioners also benefit from a higher standard deduction, raised from ₹15,000 to ₹25,000.

2. Retirement Planning: NPS Gets More Generous

One of the more overlooked but financially significant changes in recent budgets concerns the National Pension System (NPS). Under the new tax regime, the employer’s contribution to NPS is now deductible up to 14% of basic salary under Section 80CCD(2), up from the earlier 10% — a change carried forward and reinforced in Budget 2026. This deduction is one of the very few that survive under the new regime, making employer-structured NPS contributions an important lever for tax-efficient compensation structuring.

For those filing under the old regime, the familiar NPS deduction structure continues: up to ₹1.5 lakh under Section 80CCD(1) within the overall Section 80C limit, plus an additional ₹50,000 under Section 80CCD(1B) — a combined potential deduction of ₹2 lakh purely from retirement contributions, before counting the employer’s 80CCD(2) benefit.

- New regime: Employer NPS contribution deductible up to 14% of basic salary (Section 80CCD(2)).

- Old regime: Up to ₹1.5 lakh under Section 80CCD(1), plus ₹50,000 under Section 80CCD(1B).

- NPS withdrawal norms have also been liberalised — up to 100% of the corpus can now be withdrawn at maturity if the total corpus is ₹8 lakh or below, and up to 80% if the corpus exceeds this threshold, compared to the earlier 60% cap.

If your employer offers a flexible benefits structure, this is worth revisiting with your HR or payroll team — restructuring a portion of CTC into employer NPS contributions can lower taxable income meaningfully under the new regime, where most other deductions are unavailable.

3. The New Income Tax Act, 2025: A Generational Shift

Perhaps the most consequential change in Budget 2026 is the activation of the Income Tax Act, 2025, effective April 1, 2026. This new legislation replaces the Income Tax Act, 1961 — a document that had accumulated 64 years of amendments, circulars, and legal complexity, frequently cited as one of the most litigated tax statutes in the world.

It is worth noting an important transition detail: although the Income Tax Act, 2025 takes effect from April 1, 2026, the provisions of the 1961 Act continue to apply for Assessment Year 2026-27, since that assessment year pertains to income earned up to March 31, 2026. In practical terms, the new Act governs income earned from April 2026 onwards — meaning its real impact will first be felt when filing returns for FY 2026-27 in the 2027 filing season.

The New Income Tax Rules, 2026, issued by the Central Board of Direct Taxes, also came into force from April 1, 2026. Alongside updated deduction limits and revised PAN requirements, the terminology itself is modernised: the familiar terms ‘Financial Year’ and ‘Assessment Year’ are replaced by a single unified concept — the ‘Tax Year’ — reducing confusion for ordinary filers who have long struggled with the distinction.

The stated objective behind the new Act is to simplify language, reduce interpretational disputes, and cut down on litigation that has clogged India’s tax tribunals and courts for decades. Whether this translates into fewer disputes in practice will only become clear over the next few assessment cycles, but the structural intent — a cleaner, more readable tax code — is a meaningful step forward.

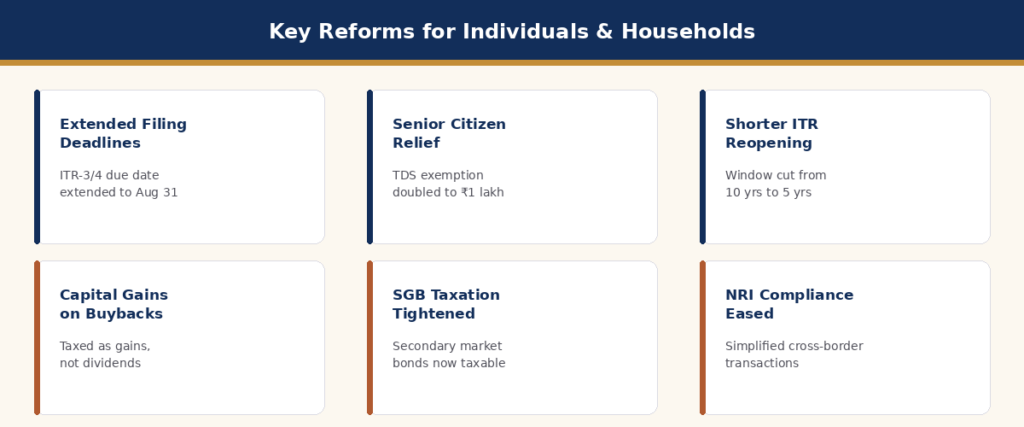

4. Key Reforms for Individuals & Households

Budget 2026 introduced a series of targeted reforms that affect specific segments of the taxpaying population. The table below summarizes the most relevant changes:

| Reform | Detail |

| Extended Filing Deadlines | ITR-3 and ITR-4 for non-audit taxpayers extended to August 31. ITR-1 and ITR-2 remain due on July 31. |

| Senior Citizen TDS Relief | Tax deduction limit under Section 80TTB doubled from ₹50,000 to ₹1 lakh — meaningful relief on deposit interest income. |

| Higher Exemption for 80+ (Old Regime) | Super senior citizens (above 80 years) get a basic exemption limit of ₹5 lakh under the old regime, versus ₹2.5 lakh standard. |

| Shorter ITR Reopening Window | Time to reopen past returns cut from 10 years to 5 years (where income escaping assessment exceeds ₹50 lakh). |

| Updated Return with Reassessment | Updated returns can now be filed even where reassessment proceedings have been initiated, subject to an additional 10% tax. |

| Capital Gains on Buybacks | From April 2026, buyback proceeds taxed as capital gains — not deemed dividends. Individual promoters: 30%, corporate promoters: 22%. |

| SGB Taxation Tightened | Capital gains exemption on maturity applies only to bonds bought during initial issue. Secondary market SGB gains now taxed. |

| TDS on RBI Floating Rate Bonds | Interest exceeding ₹10,000/month on RBI Floating Rate Bonds now attracts TDS. |

| NRI Compliance Simplified | Cross-border personal, property, and investment transactions for NRIs eased with reduced friction. |

| STT Rates Increased | STT on futures raised to 0.05% from 0.02%. STT on options raised to 0.15% from 0.10–0.125%, effective from FY 2026-27. |

| Penalty for Misreporting Eased | Tax rate on certain misreporting offences reduced from 60% to 30%; the additional 10% penalty has been omitted (200% misreporting penalty still applies separately). |

| Minimum Alternate Tax (MAT) Cut | MAT reduced from 15% to 14% from tax year 2026-27 onwards, though MAT credit cannot be set off if continuing under the old regime. |

5. Impact on Investors and Traders

Budget 2026 carries several implications for market participants, ranging from casual mutual fund investors to active derivatives traders. These changes deserve close attention, as they directly affect transaction costs and post-tax returns.

Higher Securities Transaction Tax (STT)

Effective from FY 2026-27, the Securities Transaction Tax on futures transactions has been raised to 0.05% from 0.02%, while STT on options transactions has been increased to 0.15% from the earlier 0.10–0.125% band. For frequent F&O traders, this materially raises the cost of every transaction and should be factored into strategy and position-sizing decisions, particularly for high-frequency or intraday strategies where margins are already thin.

Sovereign Gold Bonds: A Narrower Tax Exemption

Sovereign Gold Bonds (SGBs) have long been a tax-efficient way to gain exposure to gold, with capital gains at maturity fully exempt from tax. Budget 2026 tightens this: the exemption on redemption gains now applies only to bonds purchased during their original issue window. Investors who bought SGBs from the secondary market — often at a premium during periods of high demand — will now be liable to capital gains tax on those holdings. This closes what had become a popular arbitrage strategy and changes the calculus for anyone planning to buy SGBs outside of fresh issuances.

Buyback Proceeds Now Taxed as Capital Gains

From April 1, 2026, amounts received by shareholders from share buybacks will be taxed as capital gains rather than deemed dividends. For individual promoters and large shareholders, this translates to an effective tax rate of 30%, while corporate promoters face a 22% rate. This is a meaningful shift in how exit proceeds from buybacks are taxed and should be factored into corporate action planning by promoters and large institutional holders alike.

RBI Floating Rate Bonds: New TDS Trigger

Interest income on RBI Floating Rate Bonds exceeding ₹10,000 per month will now attract TDS. Retail investors who have parked significant sums in these instruments — popular for their inflation-linked, government-backed returns — should account for this withholding when projecting net cash flows.

6. Beyond Income Tax: GST, Customs & Sector Reforms

While personal income tax dominates household attention, Budget 2026 also carried indirect tax and sectoral reforms with downstream effects on prices, insurance affordability, and the cost of imported goods — all of which feed into personal finance decisions.

GST Simplification

- Section 13(8)(b) of the IGST Act has been omitted; the place of supply for intermediary services is now determined by the location of the recipient, aligning India’s rules with international norms and benefiting export-oriented service businesses.

- Conditions for issuing credit notes on post-supply discounts have been simplified — a prior agreement or invoice linkage is no longer mandatory, provided the recipient reverses the proportionate input tax credit.

- A National Appellate Authority for Advance Ruling (NAAR) is being established from April 1, 2026 to bring consistency to GST advance rulings across states.

Customs Duty: Personal Imports Get Cheaper

In a change with direct relevance to households, the Basic Customs Duty (BCD) rate on dutiable goods imported for personal use has been reduced from 20% to 10%, effective April 1, 2026. This makes personal imports — electronics, gadgets, and other goods bought from overseas for personal consumption — meaningfully cheaper. Separately, the budget also extends full customs duty exemption to 36 lifesaving drugs and medicines, a direct relief for patients managing chronic or critical illnesses.

Insurance Sector: Higher Foreign Investment Limit

The FDI limit for the insurance sector has been raised from 74% to 100%. While this is a structural, capital-markets-level change, it is expected to increase competition and capital inflow into the Indian insurance industry over time — potentially translating into more product choice and competitive pricing for policyholders, though such effects typically take a few years to filter through to retail consumers.

Startups, Manufacturing & Strategic Sectors

- The window for startups to incorporate and avail tax benefits has been extended until April 1, 2030, giving founders a longer runway to qualify for incentives.

- A presumptive taxation regime has been introduced for non-residents engaged in electronics manufacturing, aimed at boosting India’s position in global electronics supply chains.

- A Deep Tech Fund of Funds has been launched to support next-generation startups in frontier technology areas.

- An Urban Challenge Fund of ₹1 lakh crore has been set up for city redevelopment projects — a long-horizon infrastructure commitment relevant to anyone tracking urban real estate and municipal investment trends.

7. Old vs New Regime: Which One Wins for You?

The regime choice remains the most consequential personal finance decision for FY 2026–27, and Budget 2026’s lack of slab changes means last year’s calculus largely still holds. As a practical rule of thumb: taxpayers claiming deductions exceeding ₹3.5–4 lakh annually — such as home loan interest, HRA, Section 80C investments (PPF, ELSS, life insurance), and health insurance premiums under Section 80D — may still find the old regime more beneficial. For those without such deductions, or with incomes below ₹15 lakh, the new regime’s lower rates almost always win.

It is worth remembering that the new tax regime does still permit a small set of deductions, despite its ‘no exemptions’ reputation: the standard deduction of ₹75,000, employer’s NPS contribution under Section 80CCD(2) up to 14% of salary, deduction for additional employee cost under Section 80JJAA, and exemptions on gratuity, leave encashment, and voluntary retirement payouts. What it does not permit is HRA, Section 80C, Section 80D, and home loan interest on a self-occupied property — the deductions that typically matter most to salaried, middle-income households with active investment and insurance portfolios.

Approximate Tax Comparison by Income Level

| Income | Old Regime | New Regime | Savings | Who Benefits |

| ₹10 Lakh | ₹1,12,500 | NIL | ₹1,12,500 | Most salaried |

| ₹15 Lakh | ₹2,57,400 | ₹97,500 | ₹1,59,900 | Middle income |

| ₹20 Lakh | ₹4,13,400 | ₹1,92,400 | ₹2,21,000 | Upper-middle |

| ₹25 Lakh | ₹5,69,400 | ₹3,19,800 | ₹2,49,600 | HNI / Exec |

| ₹30 Lakh | ₹7,25,400 | ₹4,75,800 | ₹2,49,600 | High earners |

* Approximate figures assuming no deductions under the old regime. Actual savings under the old regime increase if you claim HRA, 80C, 80D, and home loan interest. Consult your Financial Advisor for personalized calculations.

A Quick Decision Framework

- If your total eligible deductions (80C + 80D + HRA + home loan interest) exceed ₹4 lakh annually → the old regime likely wins.

- If you have minimal deductions, no home loan, and rent isn’t a major expense → the new regime almost always wins.

- If you’re unsure, calculate both ways using an online tax calculator before submitting your regime declaration to your employer in April — switching mid-year isn’t possible for salaried employees, though you can choose differently at the time of filing your ITR.

- Business income earners face a stricter rule: switching between regimes is allowed only once in a lifetime if you have business or professional income, so this decision carries more weight for the self-employed and freelancers.

8. Your Personal Finance Checklist for FY 2026–27

Taxpayers should act on the following immediately to make the most of Budget 2026’s provisions:

- Compare old vs new tax regime before April and inform your employer of your choice; remember salaried employees can revisit this choice annually, but business-income earners cannot switch freely.

- Salaried employees: ₹75,000 standard deduction is automatic under the new regime — no separate claim needed.

- Review your CTC structure with HR — employer NPS contributions up to 14% of basic salary remain deductible even under the new regime.

- Senior citizens: leverage the enhanced ₹1 lakh TDS exemption on interest income under Section 80TTB.

- Super senior citizens (80+) considering the old regime should note the higher ₹5 lakh basic exemption limit available to them.

- Holding Sovereign Gold Bonds from secondary markets? Understand the new capital gains tax rules before planning an exit.

- F&O traders: factor in higher STT rates (0.05% on futures, 0.15% on options) when reviewing trading costs from April 2026.

- Promoters or large shareholders expecting a buyback: plan for capital gains tax treatment — 30% for individuals, 22% for corporates.

- File ITR-1 / ITR-2 by July 31, 2026. ITR-3 / ITR-4 (non-audit) by August 31, 2026.

- Ensure your Aadhaar is valid and linked — enrollment IDs no longer accepted for ITR/PAN.

- NRIs: review simplified procedures for property transactions and LRS remittances.

- Planning a personal import from abroad? The reduced Basic Customs Duty (20% to 10%) makes this a better time to bring in higher-value personal goods.

9. The Bigger Picture

Budget 2026 is best understood as a budget of consolidation rather than disruption. The sweeping relief introduced in Budget 2025 — zero tax up to ₹12 lakh, an enhanced Section 87A rebate, and the revised slab structure — has been locked in and extended rather than re-engineered. The new Income Tax Act anchors these changes in a simplified legal framework built for the next generation of taxpayers, even though its real-world effects will only become visible once it governs a full assessment cycle starting FY 2026-27.

Beyond income tax, the budget’s quieter moves — the STT hike on derivatives, the narrowing of SGB tax exemptions, the customs duty cut on personal imports, and the higher FDI ceiling for insurers — collectively nudge household financial behaviour in specific directions: towards long-only equity exposure over high-frequency trading, towards primary-market gold bonds over secondary-market arbitrage, and towards a more open, competitive insurance marketplace over time.

For the middle-income household, the message from North Block is clear: the government is betting that higher disposable incomes will drive consumption, savings, and investment, fuelling India’s domestic demand engine even as global trade becomes increasingly uncertain. Whether this bet pays off will depend as much on execution as on policy design — but for the individual taxpayer filing returns this July, the reforms offer both relief and clarity.

The government estimates a revenue foregone of nearly ₹1 lakh crore in direct taxes — a historic commitment to putting money back in the hands of India’s taxpayers, even as it simultaneously tightens compliance and closes specific tax-arbitrage windows elsewhere in the system.

WealthTech Speaks or any of its authors are not responsible for any errors or omissions, accuracy, completeness, timeliness or for the results obtained from the use of this information. This article is for informational purpose only. Readers are advised to research further to have detailed knowledge on the topic. It is very important to do your own analysis and consult your Financial Advisor before arriving at any conclusion.

Categories

- All About Mutual Funds (20)

- Annual Budget (14)

- Banner (6)

- Bonus Act (1)

- Economic Trends (38)

- Economy (52)

- Employee Deposit Linked Insurance Scheme (EDLI) (1)

- Employees’ Benefits (37)

- Employees’ Pension Scheme (EPS) (11)

- Employees’ Provident Fund (EPF) (13)

- Employees’ State Insurance (ESI) (4)

- Equity Linked Savings Scheme (ELSS) (12)

- Gadgets Review (70)

- Gratuity Act (4)

- Health Insurance (10)

- Home Loans (5)

- HR Talks (6)

- Human Resource (18)

- Income Tax (69)

- Indirect Tax (1)

- Insurance (28)

- Investment Plans (55)

- Investments (74)

- Life Insurance (22)

- Loans (6)

- Mutual Funds (30)

- Other HR Laws (7)

- Personal Loans (4)

- Portfolio Management (14)

- Portfolio Management (7)

- Professional Tax (9)

- Retirement Benefits (14)

- Retirement Plans (22)

- SidebarAd (1)

- Statutory Benefits (19)

- Systematic Investment Plan (SIP) (7)

- Tax Planning (40)

- Taxation (77)

- Tech News (22)

- Technology (81)

- Wages Act (3)

- Wealth Speaks...!!! (66)