Small Savings Scheme Interest Rates Q2 FY 2026-27

- Posted By Amritesh

- On July 15th, 2026

- Comments: no responses

If you invest in the Public Provident Fund (PPF), Senior Citizen Savings Scheme (SCSS), Sukanya Samriddhi Yojana (SSY), National Savings Certificate (NSC), or any Post Office savings scheme — this is your essential quarterly update.

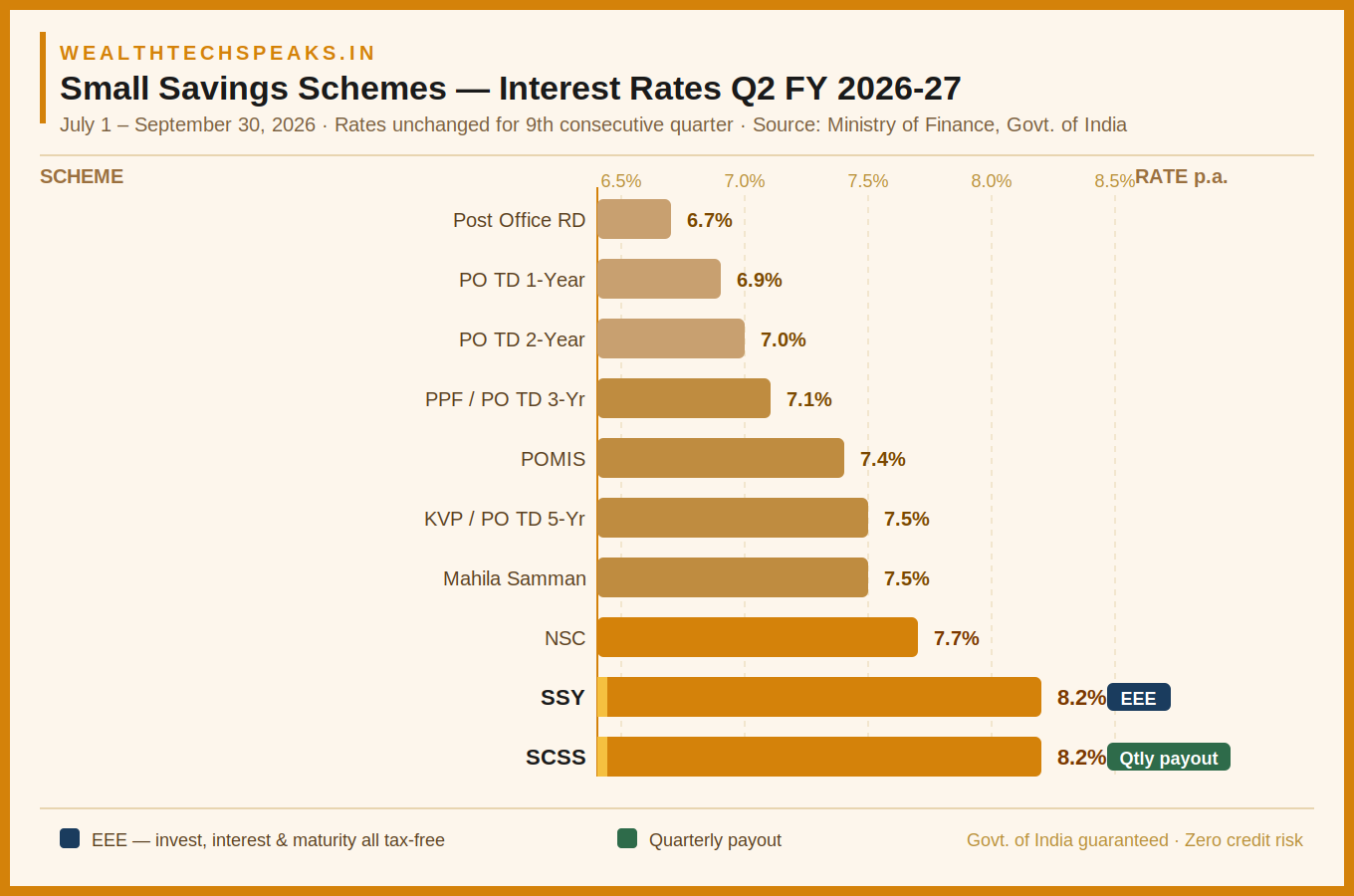

On June 30, 2026, the Department of Economic Affairs (Ministry of Finance) issued a notification confirming that small savings scheme interest rates for Q2 FY 2026-27 — covering July 1 to September 30, 2026 — remain completely unchanged from the previous quarter.

Key Highlights

- The complete interest rate table for all 13 small savings schemes

- A detailed side-by-side comparison of the most popular schemes

- An investor profile guide — which scheme suits whom

- An 8-question FAQ addressing the most common queries

- Context on why rates have been frozen for nine consecutive quarters

Complete Small Savings Scheme Interest Rates Table — Q2 FY 2026-27 (July–September 2026)

The table below lists all major government small savings schemes with their current interest rate, tenure, eligibility, and tax treatment effective from July 1, 2026.

| Scheme | Eligible For | Rate | Tenure | Sec 80C | Interest Mode |

| Sukanya Samriddhi Yojana (SSY) | Girl child below 10 yrs | 8.2% | 21 yrs / till age 18 | Yes (EEE) | Annual lump sum |

| Senior Citizen Savings Scheme (SCSS) | Age 60+ (or 55 on VRS) | 8.2% | 5 yrs + 3 yr ext. | Yes | Quarterly payout |

| National Savings Certificate (NSC) | Any resident Indian | 7.7% | 5 years | Yes | Annual (accrual) |

| Post Office TD – 5 Year | Any resident Indian | 7.5% | 5 years | Yes | Annual payout |

| Kisan Vikas Patra (KVP) | Any resident Indian | 7.5% | 115 months | No | Doubles at maturity |

| Mahila Samman Savings Certificate | Women & girls | 7.5% | 2 years | No | Quarterly |

| Post Office MIS (POMIS) | Any resident Indian | 7.4% | 5 years | No | Monthly payout |

| Public Provident Fund (PPF) | Any resident Indian | 7.1% | 15 yrs (extendable) | Yes (EEE) | Annual lump sum |

| Post Office TD – 3 Year | Any resident Indian | 7.1% | 3 years | No | Annual payout |

| Post Office TD – 2 Year | Any resident Indian | 7.0% | 2 years | No | Annual payout |

| Post Office TD – 1 Year | Any resident Indian | 6.9% | 1 year | No | Annual payout |

| Post Office RD (5 Year) | Any resident Indian | 6.7% | 5 years | No | Maturity |

| Post Office Savings Account | Any resident Indian | 4.0% | On-demand | No | Annual |

* EEE: Exempt on Investment, Exempt on Interest, Exempt on Maturity. ETE: Exempt Investment, Taxable Interest, Exempt Maturity.

Why Have Small Savings Scheme Interest Rates Not Changed for 9 Consecutive Quarters?

Small savings scheme interest rates are linked to Government Securities (G-Sec) yields through a formula recommended by the Shyamala Gopinath Committee. Specifically, each scheme’s rate is benchmarked to the yield on G-Secs of comparable tenure, with a spread of 0 to 100 basis points added on top.

However, the government is not legally required to revise rates every quarter. The current freeze reflects a deliberate policy stance driven by several factors:

- G-Sec yields have remained range-bound, providing no strong trigger for a rate change

- The government is balancing the fiscal cost of high small savings rates against the need to protect millions of small savers

- Stability in small savings rates reduces uncertainty for senior citizens and pensioners who depend on SCSS and POMIS income

- The RBI has maintained a cautious monetary stance, making large rate revisions in either direction unlikely

The last revision in small savings rates took place in Q4 of FY 2023-24, when rates for a few schemes were marginally increased. Since then, nine consecutive quarters have passed without any change.

Detailed Comparison: PPF vs NSC vs SCSS vs SSY

These four schemes are the most widely used across Indian households. The comparison below covers all key parameters to help you decide which scheme best fits your financial goal, tax situation, and investment horizon.

| Feature | PPF | NSC | SCSS | SSY |

| Interest Rate | 7.1% | 7.7% | 8.2% | 8.2% |

| Tax Status | EEE | ETE | ETT | EEE |

| Eligibility | Any Indian | Any Indian | Age 60+ only | Girl child <10 yrs |

| Min. Investment | ₹500/yr | ₹1,000 | ₹1,000 | ₹250/yr |

| Max. Investment | ₹1.5 lakh/yr | No limit | ₹30 lakh | ₹1.5 lakh/yr |

| Tenure | 15 yrs (ext.) | 5 years | 5+3 yrs | 21 yrs / till 18 |

| Tax on Interest | Exempt | Taxable (accrual) | Taxable (TDS >₹50K) | Exempt |

| Tax on Maturity | Exempt | Taxable | Taxable | Exempt |

| Premature Exit | Partial after yr 7 | Not allowed | With penalty | Death/illness only |

| Loan Facility | Yes (yr 3 onward) | As collateral | No | No |

| Interest Payout | At maturity | At maturity | Quarterly | At maturity |

| Best For | Long-term corpus | Fixed 5-yr lock | Retirement income | Daughter’s future |

Comparison: KVP vs POMIS vs Post Office Recurring Deposit

These three schemes serve investors looking to double a lump sum (KVP), generate monthly income (POMIS), or build savings systematically through monthly deposits (RD). None of these offer a Section 80C deduction.

| Feature | KVP | POMIS | Post Office RD |

| Interest Rate | 7.5% | 7.4% | 6.7% |

| Tenure | 115 months | 5 years | 5 years |

| Min. Investment | ₹1,000 | ₹1,000 | ₹100/month |

| Max. Investment | No limit | ₹9L (single) / ₹15L (joint) | No limit |

| Money Doubles In | ~9.6 years | N/A | N/A |

| Interest Mode | Doubles at maturity | Monthly payout | At maturity |

| Section 80C | No | No | No |

| Premature Exit | After 2.5 yrs | After 1 yr (penalty) | After 3 years |

| Best For | Lump sum doubling | Monthly income | Monthly savings habit |

Which Small Savings Scheme Is Right for You? — Investor Profile Guide

Young Professional (Age 25–35)

- Start a PPF account immediately if you have not already. The 15-year lock-in works in your favour — compounding at 7.1% tax-free builds a substantial corpus by retirement.

- If you have a daughter below age 10, open an SSY account. At 8.2% EEE, it is the single best guaranteed return available in India.

- NSC can fill your remaining ₹1.5 lakh 80C basket for short 5-year lock-ins, but factor in the annual tax on accrued interest.

Middle-Aged Investor (Age 40–55)

- Keep your PPF active — every extended block of 5 years adds to the tax-free corpus.

- For surplus lump sums beyond your 80C limit, KVP at 7.5% is a clean, no-documentation doubling instrument.

- Begin building a POMIS corpus now so that monthly payouts start when you need them post-retirement.

Senior Citizen (Age 60+)

- SCSS should be your first priority. At 8.2% with quarterly payout, a ₹30 lakh deposit generates approximately ₹61,500 every quarter (before tax).

- Pair SCSS with POMIS for monthly income to cover regular household expenses.

- The 5-year Post Office TD at 7.5% offers a Section 80C benefit and is suitable for parking surplus FD maturities.

Parent of a Daughter (Any Age)

- SSY is non-negotiable. Open the account as early as possible — ideally when your daughter is between 0–5 years. The longer the investment horizon, the larger the tax-free maturity corpus at 8.2% p.a.

- Maximum investment: ₹1.5 lakh per financial year. Even ₹12,500 per month adds up to a significant sum over 14–15 years.

Salaried Taxpayer (30% Bracket)

- Maximise Section 80C first using PPF or 5-Year Post Office TD before deploying into non-80C instruments.

- Avoid NSC if the annual taxable accrual will push you into a higher tax bracket or create unnecessary ITR complexity.

- SCSS (if 60+) or KVP are clean choices for lump-sum deployment outside the 80C window.

Frequently Asked Questions (FAQs)

Below are the most commonly searched questions on small savings scheme interest rates for Q2 FY 2026-27.

| Question | Answer |

| Have small savings rates changed for July–September 2026? | No. The Ministry of Finance confirmed on June 30, 2026 that all small savings scheme interest rates remain unchanged for Q2 FY 2026-27. This is the ninth consecutive quarter without a revision. |

| Which scheme offers the highest interest rate in 2026? | SSY and SCSS both offer 8.2% p.a. — the highest among all small savings schemes. SSY is restricted to girl children (below age 10) while SCSS is available only to senior citizens (age 60+). |

| Is PPF a good investment at 7.1% when bank FDs offer similar rates? | Yes. PPF’s key advantage is its EEE tax status — contributions, interest, and maturity are all fully tax-exempt. A 7.1% PPF return is effectively superior to a 7.5% bank FD for a taxpayer in the 30% slab. |

| When does the government revise small savings scheme interest rates? | Rates are reviewed every quarter (April–June, July–September, October–December, January–March). However, revision is not compulsory — the government may keep rates unchanged, as it has done for nine consecutive quarters. |

| Is SCSS interest taxable? | Yes. SCSS interest is fully taxable per your income tax slab. TDS at 10% applies if interest exceeds ₹50,000 in a year. However, senior citizens can claim up to ₹50,000 interest deduction under Section 80TTB. |

| In how many months does KVP double your money? | At the current rate of 7.5%, KVP doubles your investment in 115 months (approximately 9 years and 7 months). |

| Can I open a PPF account for my minor child? | Yes. A parent or guardian can open and manage a PPF account for a minor. The combined investment limit of ₹1.5 lakh per year applies across both the parent’s and child’s PPF accounts. |

| Which scheme is best for monthly income after retirement? | POMIS (7.4%) and SCSS (8.2%) are the two best options. SCSS offers a higher rate with quarterly payout while POMIS pays monthly. Many retirees use both for complementary cash flow. |

The Bottom Line….

Small savings schemes backed by the Government of India continue to be one of the safest and most reliable investment options available to Indian investors. Despite nine consecutive quarters of unchanged rates, small savings scheme interest rates remain highly competitive — particularly SSY (8.2%) and SCSS (8.2%) — especially when compared against bank fixed deposits that are under pressure from the ongoing rate cycle.

The key takeaway for Q2 FY 2026-27 is this: stay invested, keep your PPF active, maximise SSY if you are eligible, and prioritise SCSS if you are a senior citizen.

This article is for informational purpose only. Readers are advised to research further to have more clarity on the topic. It is very important to do your own analysis and consult your Financial Advisor before making any investment based decision.

Categories

- All About Mutual Funds (20)

- Annual Budget (14)

- Banner (6)

- Bonus Act (1)

- Economic Trends (38)

- Economy (51)

- Employee Deposit Linked Insurance Scheme (EDLI) (1)

- Employees’ Benefits (37)

- Employees’ Pension Scheme (EPS) (11)

- Employees’ Provident Fund (EPF) (13)

- Employees’ State Insurance (ESI) (4)

- Equity Linked Savings Scheme (ELSS) (12)

- Gadgets Review (70)

- Gratuity Act (4)

- Health Insurance (10)

- Home Loans (5)

- HR Talks (6)

- Human Resource (18)

- Income Tax (68)

- Indirect Tax (1)

- Insurance (28)

- Investment Plans (55)

- Investments (73)

- Life Insurance (22)

- Loans (6)

- Mutual Funds (29)

- Other HR Laws (7)

- Personal Loans (4)

- Portfolio Management (14)

- Portfolio Management (7)

- Professional Tax (9)

- Retirement Benefits (14)

- Retirement Plans (22)

- SidebarAd (1)

- Statutory Benefits (19)

- Systematic Investment Plan (SIP) (7)

- Tax Planning (40)

- Taxation (76)

- Tech News (22)

- Technology (81)

- Wages Act (3)

- Wealth Speaks...!!! (65)